Briefing Paper

Running up that hill: The WTO’s battle with modern industrial policy

Fetzer, T; Martinez, A; and Zhangyue, T. (2026) Running up that hill: The WTO’s battle with modern industrial policy, CITP Briefing Paper 32

Published 25 June 2026

CITP Briefing Paper 32

Key points

- Industrial policy is converging and fragmenting simultaneously. Analysis of G7 and Chinese industrial-policy documents shows broad agreement on the top objectives and the policy tools each country intends to deploy. Yet “Frontier Tech & AI,” arguably the single most consequential objective, is precisely the one where countries diverge most in their language.

- The system offers no protection against coercive bilateral pressure dressed up as reciprocal trade. The US–Indonesia deal (early 2026) illustrates the asymmetry: under tariff threats, Indonesia dismantled nearly two decades of downstream minerals-processing strategy in exchange for a tariff cut from 32% to 19% that mostly benefits Indonesian agriculture.

- The WTO’s mid-century rulebook is increasingly unenforceable against modern industrial policy. The Subsidies and Countervailing Measures (SCM) Agreement disciplines rather than prohibits subsidies, but today’s strategic, green, and security-linked subsidies routinely escape scrutiny through legal framing and political justification.

- A dysfunctional WTO serves powerful members’ strategic interests. As a digital-services exporter, the US benefits from bilateralising negotiations to maximise leverage, pre-wiring permanent duty-free digital commitments through bilateral deals while pressing for bans on digital services taxes and data-localisation mandates. Most member states’ digital trade policy instruments are in fact aimed at protecting domestic AI development and/or extracting revenue from the digital economy rather than facilitating cross-border digital commerce.

- The realistic path for keeping the WTO relevant in an era of modern industrial policy is transparency and plurilateral coordination, not wholesale reform. Wholesale reform is politically unrealistic: major economies will not abandon strategic subsidies or security exceptions, and smaller economies cannot win a subsidy race. The priority should instead be clarifying genuine security exceptions, setting reporting thresholds, and embedding transparency.

The enforcement problem

The WTO’s Subsidies and Countervailing Measures (SCM) Agreement disciplines subsidies but does not prohibit them outright; instead, it relies on categories and enforcement mechanisms designed for an earlier era.1 Today’s industrial policy routinely bypasses these categories through legal framing and political justification. This is most visible in the case of green, strategic, and security-linked subsidies, though many other tools are intentionally opaque or structured to avoid scrutiny. More broadly, it is the combination of arbitrariness and flexibility without transparency that makes the WTO’s mandate difficult to enforce and increasingly irrelevant.

This erosion of enforceability is compounded by the paralysis of the dispute settlement system following the suspension of Appellate Body appointments, further hollowing out the WTO’s role as a credible arbiter of global trade rules. Current industrial policies occupy a peculiar space: enforcement is technically possible under the SCM Agreement, but diplomatically impossible because every major economy is engaged in similar practices. The new wave of strategic subsidies (e.g., US EV and IRA credits, EU local-content mandates, Japanese semiconductor support, and recent UK procurement policies) are openly justified as responses to climate, security, or resilience concerns.2 On paper, they are subject to WTO discipline. In practice, their framing shields them from enforcement, and reciprocal behaviour makes formal challenges politically infeasible. The result is a grey zone in which systemic tensions accumulate as all major economies operate under the same logic.

The new landscape of trade in goods

Modern industrial policy in goods is increasingly justified through climate objectives, supply-chain protection, and national security. These three rationales are frequently bundled together and mutually reinforcing. Carbon pricing and CBAM mechanisms illustrate the first: 75 carbon tax and trading schemes are now in operation worldwide, with the UK set to introduce its own CBAM in 2027.3 These tools aim to reduce carbon leakage, but political bargaining and uneven implementation expose the risk of fragmentation. The collapse of the Global Arrangement on Sustainable Steel and Aluminium (GASSA) is a case in point of how such bargaining can fragment carbon policy.4

Where carbon tools fall short, green and strategic subsidies have stepped in as the preferred alternative to tariffs for responding to shocks and building domestic capacity. But a subsidy race carries a distributional cost: it risks marginalising smaller and poorer economies that lack the fiscal space to compete, potentially shutting them out of both decarbonisation efforts and global market access. It is not only distributionally costly but potentially a prisoners' dilemma, where the social costs are too high for everyone involved.5

The third and most contested frontier is supply-chain control. China’s near-monopoly in rare earths and key minerals, alongside its willingness to weaponise supply chains, has shifted Western industrial policy toward securing inputs rather than merely boosting production. US-Japan coordination and EU-Serbia resource initiatives reflect this logic.6 But the costs of this scramble fall unevenly. The US-Indonesia trade deal finalised in early 2026 illustrates the asymmetry starkly: Indonesia had spent nearly two decades building a downstream minerals processing strategy to secure a position in the global battery supply chain. Under pressure from US tariff threats, it effectively dismantled that strategy in exchange for a reduced tariff rate, from 32 to 19%, mostly benefiting its agricultural sector, lifting export restrictions on critical minerals, waiving local content requirements for US companies, and effectively conceding defeat on its efforts to develop its own tech stack. Here the issue is not that the WTO lacks a framework, since the Most Favoured Nation (MFN) principle applies, but that it is routinely ignored.

Energy security follows the same logic. When Russia curtailed gas supplies to Europe following its invasion of Ukraine in 2022, the US stepped in as Europe’s primary liquified natural gas supplier. The Trump administration has been explicit about using this dependency as bargaining power, with Europe purchasing approximately $80 billion in US energy in 2024.7 Canada, which might have provided an alternative supply source, declined to build the necessary East Coast infrastructure in 2022. This missed opportunity has left Europe with fewer options and greater exposure to US pressure, which it most recently felt again after the US-induced military action in Iran. Like critical minerals, energy security has become an instrument of industrial policy that operates entirely outside the WTO’s current mandate.

Bottom line: Reshoring, onshoring, and protective interventions in food systems, defence industries, and critical materials have become politically untouchable, frequently justified through broad and imprecise notions of “resilience.” More troubling still, the WTO’s current mandate offers no framework to protect smaller members from the coercive pressure that major economies increasingly deploy through supply-chain dependency and bilateral trade threats.

The challenge of services and data transparency

The least governed — and hardest to measure — industrial policy frontiers now lie in services, including digital currencies, payment systems, satellite infrastructure, and data platforms. Interventions such as stablecoins, digital IDs, and Value Added Tax (VAT) traceability mechanisms raise sovereignty concerns and pose serious analytical challenges, particularly around tracking cross-border data flows, identifying implicit subsidies, and valuing digital services. The recently concluded WTO Ministerial Conference (MC14) in Yaoundé resulted in an impasse with the long-held e-commerce moratorium on there being no customs duties on electronic transmissions. Such customs duties could be acting as an implicit subsidy to data centres and could boost localisation initiatives in the services domain. Control over the infrastructure of the digital economy, both its physical and non-physical elements, is explicitly and deeply geopolitical. It touches upon key pillars around which concepts of national sovereignty are being defined. And naturally, a highly centralised supply side for digital services may enable platforms to become vectors for deep interference in societal processes. Further, governance over the raw material of the modern services economy — data — alongside its protection is subject to different legal norms and historically grown customs. High degrees of (public) data access may facilitate innovation and knowledge sharing, yet, they can also create vulnerabilities in the context of growing escalation.8

The US, for example, being an exporter of digital services, has a strong negotiation objective to attempt to bilateralise negotiations over market access for its tech giants for each country. This is precisely why a dysfunctional WTO is in the US strategic interests. Bilateralising trade relationships allows the US to maximise its negotiation power. Under Donald Trump, it has exploited other countries’ (security) vulnerabilities to, among others, impose effective bans to adopting digital service taxes that could tackle the base-erosion and profit-shifting practices that are common and may contribute to the erosion of social contracts across countries. As countries may mull industrial policy to localise data processing, the US further aims to achieve bans on data localisation mandates, which, in the worst case, would undermine the ability of legal systems to enforce their own rules and regulations. In abstract terms, such an arrangement could be read as giving the US an effective vector of influence over societies in ways that may escape accountability, while tilting the competitive field in favour of its own legal services and technology firms. This is an outcome akin to an implicit subsidy, even if it is not one in the formal sense.

This divergence matters far beyond privacy policy. Measuring digital trade requires the ability to trace digital transactions, which in turn requires robust digital identity. Protecting intellectual property in the digital economy requires shared infrastructure to establish idea provenance, de-duplicate claims, and resolve disputes. In the case of digital assets, this points toward some form of global provenance system, or shared compute and storage infrastructure that may hard-code a model of human flourishing, which, naturally may be difficult to accept for some players. Technologically, much of this is feasible and already exists in fragments. Indeed, US-based private actors are already attempting to roll out such rails. However, these systems are not neutral; rather, they are embedded in legal jurisdictions, security architectures, compliance regimes, cloud dependencies, identity layers, and AI governance systems. Access points are not merely accidental “backdoors” but may be design features of modern security architecture: lawful-access procedures, privileged administration, key-management systems, audit and monitoring tools, sanctions-compliance layers, emergency-access protocols, and intelligence-facing interfaces. For countries relying on externally-controlled infrastructure, these become channels through which foreign states may compel access, exert pressure, shape enforcement, or selectively interrupt service. AI makes this problem more fundamental still: once identity, provenance, content validation, dispute resolution, fraud detection, and knowledge production are mediated by AI systems, control over the underlying models, training data, inference infrastructure, retrieval layers, and evaluation standards becomes a form of infrastructural power. The issue is therefore not simply data privacy, but sovereignty over the systems that determine what is traceable, attributable, authentic, enforceable, and economically legible.

The measurement problem extends well beyond digital identity. There is broad consensus that weak evidence and severe data challenges have undermined the WTO’s ability to discipline modern industrial policy, particularly cumulative, indirect, and long-term interventions. China illustrates this most starkly: decades of targeted state support have so fundamentally shaped industrial capacity that it is nearly impossible to disentangle genuine market competitiveness from the legacy of sustained intervention. The WTO’s framework was never designed to adjudicate supply-chain structures built through multi-decade policy accumulation. Services remain poorly captured in national and trade statistics, digital interventions are often opaque by design, and policy frameworks compound the problem with arbitrary thresholds and vague definitions, with the EU Net-Zero Industry Act’s 40% domestic manufacturing target being a clear example.9 The use of “security” as a catch-all policy justification adds yet another layer of deliberate ambiguity.

Bottom line: The services and digital economy are ungovernable at the multilateral level not only because measurement is hard, but because key actors have a vested interest in keeping it that way. Transparency, standardisation, and clearer definitions are not merely technical fixes. They are the precondition for any credible WTO reform. On the question that matters most: who controls digital identity and therefore digital trade, the US and EU have structurally opposed interests, and no multilateral forum is currently equipped to resolve it.

What to expect from G7 and China’s industrial policy

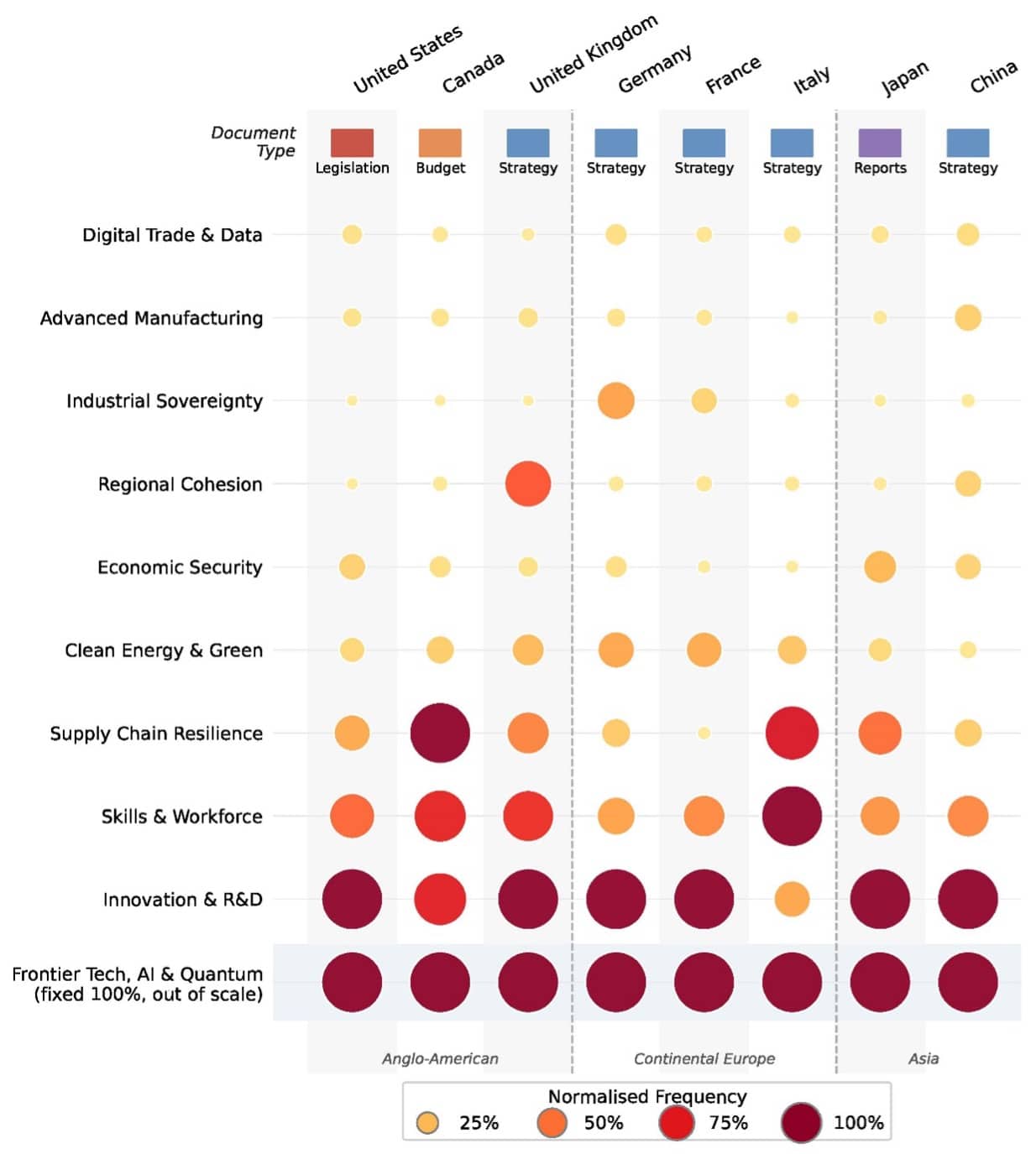

Examining industrial policy documents across the G7 countries and China provides a systematic basis for assessing the main industrial policy objectives that the world’s largest economies intend to pursue in the coming years.10 For our analysis, we construct a dictionary of policy objectives and policy terms using a large language model (LLM). We count the frequency of each objective per 1,000 words and normalise the measure within each country.11 In Figure 1, our analysis of objectives groups countries by bloc: Anglo-American, Continental Europe, and Asia. Across all countries, “Frontier Technology, AI, and Quantum” objectives appeared with disproportionately high frequency relative to all other objectives. We therefore exclude this category from the normalisation, though it should be noted that it is the most commonly referenced objective across all countries in our sample.

For all countries, “Innovation and research and development (R&D)” and “Skills and Workforce” emerge as the most prominent objectives after “Frontier Technology, AI, and Quantum”. Beyond these, the picture becomes more differentiated and a country-by-country reading is warranted, particularly given the varying nature of the documents. Among strategy documents, the UK’s main objectives, beyond those shared across the board, are “Regional Cohesion” and “Supply Chain Resilience”. Continental European countries (Germany, Italy, and France) are more focused on “Clean Energy and Green.” Canada, the US, and Japan, despite drawing on very different document types, converge on “Supply Chain Resilience” and “Clean Energy and Green” as high priorities. Finally, China references almost all objectives at meaningful intensity, with the notable exception of “Industrial Sovereignty” and, to a lesser extent, “Clean Energy and Green.”

Figure 1: Industrial Policy Objectives: Relative Importance

Notes: The figure shows the relative importance of industrial policy objectives for each G7 country and China. The top row displays the document type for each country. Bubble size reflects the relative importance of each objective within each country, measured as frequency per 1,000 words and normalised within country, excluding Frontier Technology and AI. Sources: Authors’ own estimations based on NDRC (2021); Government of Canada (2025); Government of France (2021); BMWi (2019); UK DBT (2025); Italian Government (2021); U.S. Congress (2022a,b); The White House (The White House (2018). Proclamation 9705: Adjusting imports of steel into the United States. Federal Register; and The White House (2021). Executive order 14017: America’s supply chains. Federal Register, Vol. 86, No. 39.); METI (2023a,b, 2024, 2025).

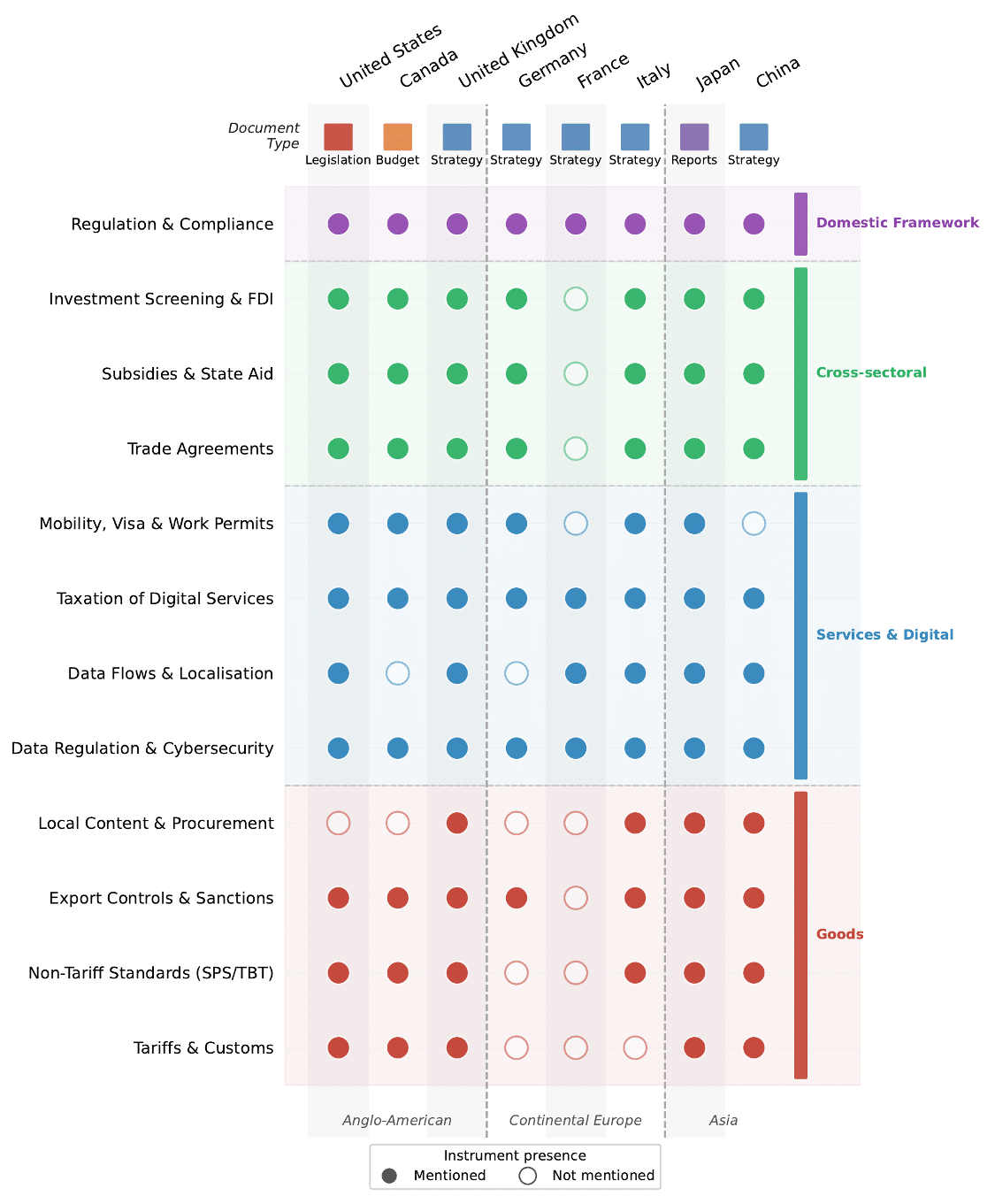

Figure 2 maps which specific policy instruments appear in the documents we reviewed.12 We show simply whether a country mentions a specific instrument or not, without assessing its importance, which allows for clean cross-country comparison of instrument presence. We classify instruments into four categories: goods trade, services and digital trade, cross-sectoral (affecting both goods and services simultaneously), and domestic framework (shaping the domestic business environment rather than trade directly).

The most striking finding is not simply a gap between objectives and instruments on digital trade; it is a misalignment of purpose. Despite “Digital Trade and Data” ranking as the least-mentioned policy objective across all countries, every country in our sample deploys instruments touching the digital economy. But on closer inspection, these instruments are not designed to govern trade in services in any WTO sense. Taxation of Digital Services, the highest-scoring instrument for the UK, Japan, France, and Germany, is primarily directed at extracting revenue from foreign technology platforms, not at facilitating cross-border digital commerce. Data regulation and cybersecurity measures are framed overwhelmingly in terms of protecting domestic AI development and national security, not cross-border data flows.

In other words, what looks like digital trade governance is, in practice, digital economy capture: countries are increasingly deploying digital industrial policy to secure domestic value capture, protect against foreign platform dominance, and build national AI capacity, while leaving the governance of trade in services largely unaddressed. This is precisely why the WTO’s services framework, the General Agreement on Trade in Services (GATS), has struggled to keep pace: the most consequential interventions in the digital economy are not framed as trade policy, and therefore fall outside the WTO’s line of sight entirely.

The picture for goods instruments requires careful interpretation. For European countries, the absence of goods trade instruments partly reflects the EU institutional architecture: tariffs, export controls, and trade agreements are EU competences and therefore do not feature prominently in national documents. France is the most extreme case of this, as discussed in footnote twelve. This means that for European economies, the most consequential goods trade instruments are embedded in EU-level frameworks that sit largely outside any single country’s industrial policy document, and therefore outside the kind of national-level transparency and accountability that domestic policy reviews attempt to capture.

Beyond this European caveat, the overall picture shows broad convergence across most instruments, with meaningful variation concentrated in a few specific tools: local content and procurement requirements (referenced by only four of the eight countries i.e., China, Italy, Japan, and the UK), data flows and localisation, and export controls and sanctions. Much like the pattern observed in services, the toolkit itself has not changed; countries still use the same instruments. What has changed is the objective they serve. Non-tariff standards, export controls and sanctions, and local content and procurement are not new instruments; they have been subject to WTO discipline for decades. But when reframed as “supply chain resilience” or “economic security” measures rather than “competitive trade policy”, they migrate out of the WTO’s lane entirely. A subsidy to domestic producers is actionable under the SCM Agreement; the same subsidy justified as a “critical mineral security” measure occupies a grey zone where challenge is legally uncertain and politically impossible. As long as resilience and security remain the dominant framing, the WTO has no effective mechanism to look behind the label.

Figure 2: Industrial Policy Instruments: Presence in Document

Notes: The figure shows whether each instrument is referenced (filled circle) or not referenced (empty circle) in each country’s industrial policy document. Instruments are grouped into four categories. Goods: tariffs and customs duties; non-tariff measures including sanitary, phytosanitary and technical barriers to trade; export controls and sanctions; and local content and public procurement requirements. Services and Digital: data regulation and cybersecurity; data flows and localisation; taxation of digital services; and mobility, visa and work permits, the latter classified here as a services instrument given its direct relevance to Mode 4 (movement of natural persons) under the GATS, though it also operates as a labour market instrument. Cross-sectoral: trade agreements (covering goods and services simultaneously); subsidies and state aid; and investment screening and FDI. Domestic Framework: regulation and compliance, referring to measures that shape the domestic business environment. Sources: Authors’ own estimations based on the documents cited above.

Finally, we examine whether countries that share an objective also share the content of how they describe it. We split each industrial-policy document into 1,000-word chunks, tag each chunk with the objectives it references (a chunk may map to more than one), and embed each chunk as a semantic vector. For every pair of countries and every objective, we compute the cosine similarity (a score from 0 to 1 capturing how similar two documents are in their word usage) of all relevant chunk pairs and aggregate to the country-pair level. We then summarise each objective with two statistics: i) the weighted mean similarity across country pairs (how similar two countries’ language tends to be when they discuss the objective); ii) the weighted standard deviation across country pairs (how much that similarity varies from one pair of countries to another).13

Figure 3 plots these two dimensions. Moving right means countries communicate the objective more alike (a shared vocabulary); moving left means more country-specific phrasing. Moving up means the (dis)similarity is uneven across pairs — driven by rival blocs of countries or, in the extreme, by a single outlier country. The lower-right thus corresponds to uniform consensus and the lower-left to uniformly idiosyncratic wording.

Mapping the objectives onto this space, “Frontier Tech & AI” is the objective on which countries diverge most in language. “Industrial Sovereignty” stands out as a topic of broad consensus punctuated by a few country outliers, and “Advanced Manufacturing” is similarly consensual but with pockets of disagreement across some country pairs. “Regional Cohesion”, “Innovation & R&D”, “Digital Trade & Tech”, and “Economic Security” are objectives on which countries communicate things most uniformly. “Supply Chain Resilience” and “Clean Energy & Green” are more contested, with fewer countries in agreement and blocs adopting distinct wordings, while “Skills & Workforce” also displays substantial dissimilarity, though of a more country-specific (rather than bloc-structured) kind. Since this latter objective remains very much a national-interest subject, such a result is unsurprising.

The substantive takeaway aligns directly with our central argument. The objectives on which countries converge on a common language in the lower-right of the figure are those where multilateral coordination is most plausible. By contrast, “Frontier Tech & AI”, arguably the single most consequential objective across our sample, is precisely the one on which countries do not agree on wording; this is where reaching consensus will be hardest and the risk of governance fragmentation is greatest. Objectives characterised by a few outliers, such as “Industrial Sovereignty”, represent exactly the kind of grey zone framing that the WTO’s current mandate is poorly equipped to discipline.

Figure 3: Topic and content dispersion of policy documents

Notes: Each point is a policy objective. The axes are the weighted mean and weighted standard deviation of country-pair cosine similarities, where each pair (A,B) is weighted the number of 1,000-word chunks the thinner of the two countries devotes to objective T; the weight discounts pair-cells in which one country has little text on the objective. Objectives in the upper-right are interpreted as topics on which most countries agree but a few do not, capturing tension between the many and the few. Pair-topic cells with fewer than 30 chunk-pair observations are dropped.

Bottom line: Industrial policy is simultaneously converging and fragmenting. Major economies agree on the instruments but deploy them in pursuit of national rather than multilateral goals. This quiet, technocratic assertion of national sovereignty, through regulatory and digital tools that sit largely outside the WTO’s current mandate, is precisely the grey zone the WTO cannot govern.

Conclusion: What is the WTO’s future?

The WTO’s mid-last-century rulebook is clearly under strain. Targeted subsidies, supply chain interventions, and green industrial policies are expanding rapidly in scale and ambition across major economies. The tension between industrial policy and WTO rules is well documented, but what is almost never discussed together is how it plays out across goods, services, and the digital economy.14 The pragmatic path forward is not to ban these policies outright or roll back security exceptions, since both of these options are politically unrealistic. Instead, the priority should be to clarify what qualifies as a genuine security exception, establish clear reporting thresholds, and embed transparency into the system. State intervention has always been permitted under WTO rules; the goal is not to eliminate national flexibility but rather to ensure it is exercised without discrimination and within a transparent, globally coordinated framework. Getting there will be an uphill battle; the alternative is governance failure on a global scale.

WTO leadership increasingly recognises the widening gap between formal rules and economic reality. The institution faces a fundamental tension: unless it evolves, global trade governance will diverge ever further from the policies actually shaping major economies.

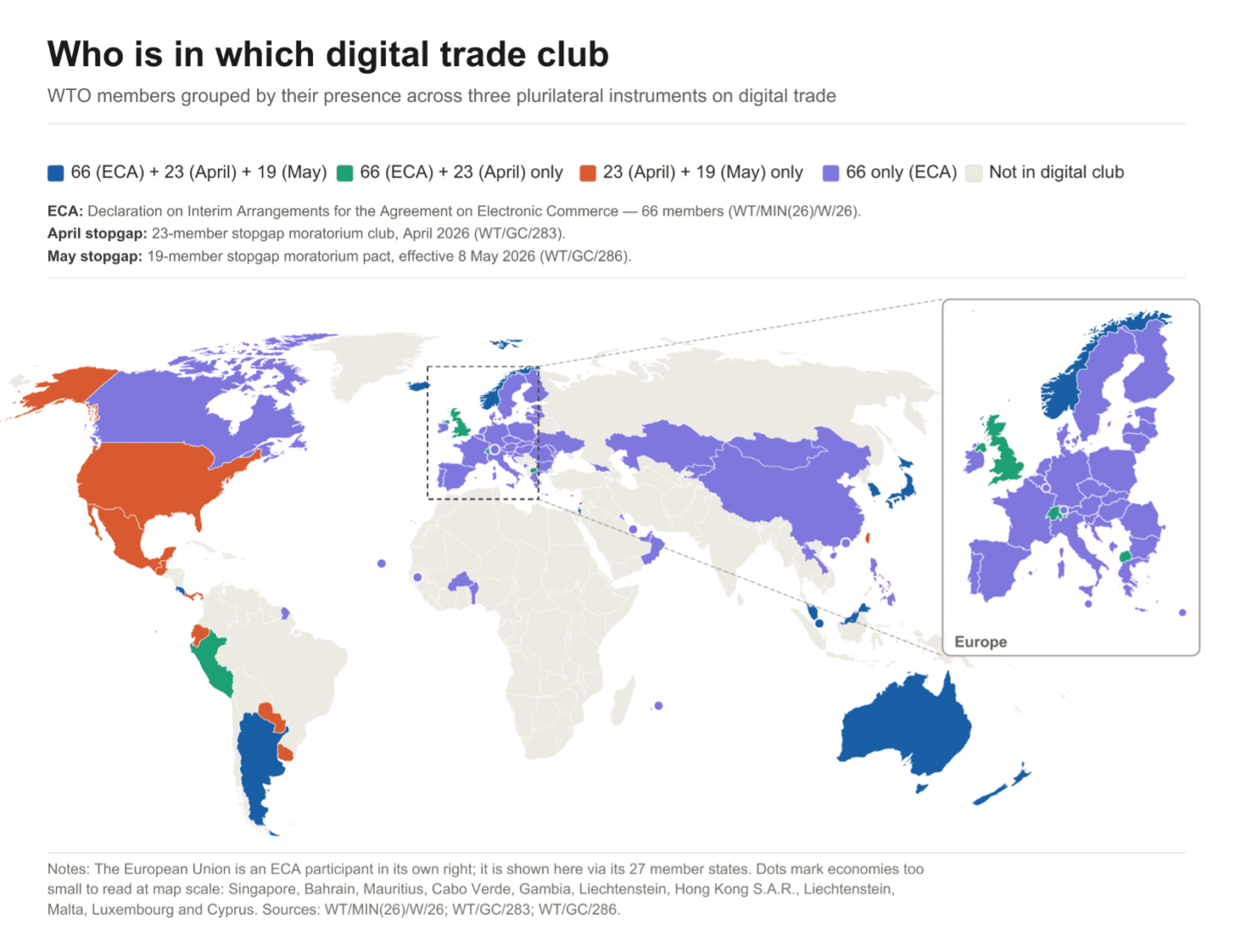

The outcome of MC14 in Yaoundé made that tension concrete. Ministers left without a final package, without an overall ministerial declaration, and without a reform work plan. With the moratorium on customs duties on electronic transmissions lapsing, sixty-six members signed a separate e-commerce agreement as a plurilateral workaround. The agreement includes the EU but not the US, meaning that the institutional authority over digital trade now rests on a substitute framework that excludes its most powerful member.

The moratorium’s lapsing matters beyond digital tariffs. Its expiry opens the political and legal space for countries to impose duties on electronic transmissions, but the deeper concern is sovereignty. The US has systematically used bilateral trade agreements to pre-wire the multilateral outcome through permanent duty-free digital trade commitments, effectively eroding the governance and oversight layer countries hold over their citizens’ data. This is not a new form of protectionism; it is a new form of hegemony, and the WTO as currently constituted has no framework to name it, let alone govern it.

Wholesale reform of the WTO is politically unrealistic. Major economies will not abandon strategic subsidies, climate investments, or security exceptions. Smaller economies cannot compete in a subsidy race. And multilateral consensus on new binding rules appears increasingly remote. The objective, therefore, is not to eliminate national flexibility or prevent countries from pursuing legitimate climate and security goals. It is to ensure these policies operate within a framework of transparency, predictability, and shared accountability. This matters especially where the playing field may not be level but is at least observable.

We close with one priority where reform could make a material difference: digital trade governance, i.e., the rules governing digital commerce and cross-border data flows. The equilibrium the world needs is not one global digital identity system or one set of platform rules; instead, what is needed is a framework in which trade in digital assets (understood broadly as any verifiable claim rendered in tradeable digital form, from identity credentials to audited carbon removals) becomes traceable and verifiable across different national architectures without requiring countries to import another country’s digital rails. Countries do not need to share the same digital infrastructure. That means common standards for verifying that transactions are traceable, taxable, and compliant across different national systems. It also means provisions on data flows, platform accountability, and digital services that preserve each country’s right to regulate, audit, and enforce domestically while keeping cross-border commerce open.

Finally, there is an open question about the institutional form the WTO should take. MC14 itself offered a partial answer: when consensus failed on the e-commerce moratorium, members moved forward with a plurilateral agreement outside the main WTO framework.15 That workaround points toward a WTO that is less a legislator of binding universal rules and more a facilitator of plurilateral coalitions among willing members, providing the legal infrastructure, transparency architecture, and dispute resolution capacity that bilateral deals cannot. This is not the WTO its founders envisioned. But it may be the WTO that the current moment makes possible: one that anchors national strategy within a shared framework of accountability; imperfectly, but transparently.

Figure 4: Who is in which digital trade club

Accessibility note: Due to technical limitations, we were unable to publish figures 1,2, and 4 in an accessible format. The data behind these figures is available on request, please contact info@citp.ac.uk

Footnotes

- World Trade Organization (1994). Agreement on subsidies and countervailing measures. Marrakesh Agreement Establishing the WTO, Annex 1A. In force 1 January 1995

- European Parliamentary Research Service (2023). The US Inflation Reduction Act: How the EU is

- World Bank (2024) State and trends of carbon pricing 2024; HM Treasury and HM Revenue & Customs (2024) Introduction of a UK carbon border adjustment mechanism from January 2027: Government response to the policy design consultation. UK Government Publication.

- Sutton, T. (2025) ‘EU’s proposed tariffs on steel to address excess capacity and enable decarbonization could worsen trade tensions’, Center on Global Energy Policy, Columbia University SIPA, 22 October.

- The United States made its objection explicit in a communication to the WTO of 15 December 2025, arguing that Members must rethink how MFN operates and re-examine its link to reciprocity.

- The White House (2025) United States–Japan framework for securing the supply of critical minerals and rare earths through mining and processing. White House Briefings & Statements; European Commission (2024) Strategic partnership on sustainable raw materials, battery value chains and electric vehicles between the European Union and the Republic of Serbia. Memorandum of Understanding, Belgrade, 19 July 2024.

- Euronews (2025) Von der Leyen and Trump strike EU-US trade deal with 15% tariff for the bloc.

- See Fetzer, T. and Schwarz, C. (2021). Tariffs and politics: Evidence from Trump’s trade wars. The Economic Journal, 131(636):1717–1741, who document how data openness interacts with strategic vulnerability.

- European Parliament and Council of the European Union (2024) Regulation (EU) 2024/1735 on establishing a framework of measures for strengthening Europe’s net-zero technology manufacturing ecosystem (Net-Zero Industry Act). In force 29 June 2024.

- This analysis draws on official government documents serving as each country’s primary industrial policy reference. For China, we use the 14th Five-Year Plan (National Development and Reform Commission of the People’s Republic of China (2021). The 14th five-year plan for national economic and social development and the long-range objectives through the year 2035. Technical report, National Development and Reform Commission); for France, the France 2030 programme (France 2030: Innover pour une France résiliente et souveraine. Technical report, France 2030 Programme); for Germany, the Industrial Strategy 2030 (German Federal Ministry for Economic Affairs and Energy (2019). Industrial strategy 2030: Guidelines for a German and European industrial policy. Technical report, Federal Ministry for Economic Affairs and Energy (BMWi)); for Italy, the National Recovery and Resilience Plan (Italian Government (2021). Piano nazionale di ripresa e resilienza (PNRR): NextGenerationItalia. Technical report, Governo Italiano.); and for the United Kingdom, the Modern Industrial Strategy (UK Government, Department for Business and Trade (2025). The UK’s modern industrial strategy. Technical Report CP 1451, Department for Business and Trade.). For Canada, which lacks a dedicated industrial strategy document, we use the 2025 Federal Budget. For the United States and Japan, where industrial policy is enacted through successive legislation and executive action rather than a single consolidated strategy, we draw on the CHIPS and Science Act, the Inflation Reduction Act, and Executive Order 14017 on supply chains for the US, and on four successive METI committee reports on the new direction of economic and industrial policy for Japan: Ministry of Economy, Trade and Industry (METI) (2023a). Interim report for committee on new direction of economic and industrial policies. Technical report, METI; (Ministry of Economy, Trade and Industry (METI) (2023b). Second report for committee on new direction of economic and industrial policies. Technical report, METI; Ministry of Economy, Trade and Industry (METI) (2024). Third report for committee on new direction of economic and industrial policies. Technical report, METI; and Ministry of Economy, Trade and Industry (METI) (2025). Fourth report for committee on new direction of economic and industrial policies. Technical report, METI)

- Cross-country comparisons are difficult because the documents are not always comparable in type or scope. The US and Japan are represented by legislation and committee reports respectively, Canada by a budget document, while the EU countries, the UK, and China have dedicated industrial strategy documents. Within-country normalisation accounts for these differences.

- France’s low instrument count reflects the nature of the France 2030 document rather than an absence of trade policy. France 2030 is an investment allocation plan that specifies where €54 billion will be deployed across sectors, rather than a trade governance strategy. Instruments such as tariffs, export controls, investment screening, and trade agreements are EU competences and therefore do not appear in French national documents. France’s instrument count should therefore be interpreted as a document scope issue rather than evidence of a thinner policy toolkit.

- Pairs are weighted by the chunk count of the thinner country on topic, so that country-pair cells in which one side has little text on the objective contribute less to the topic-level statistics.

- Bown (2023) provides a detailed account of how the new wave of strategic subsidies and industrial policy measures sits uneasily within the WTO’s existing legal framework See: Bown, C. P. (2023). Modern industrial policy and the WTO. Working Paper 23-15, Peterson Institute for International Economics.

- We provide a snapshot of the status of the digital clubs as of May 2026.

Author Profiles